Homework 6: Monday October 7, 2019

微分方程代写 Consider the so-called backward differential equation 2 2tFx t + —–x2 Fx t = 0[1.1]for a function Fx t . Rewrite this equation

Due Wednesday October 16, 2019. Total 100 points

Problem 1. [20 points] 微分方程代写

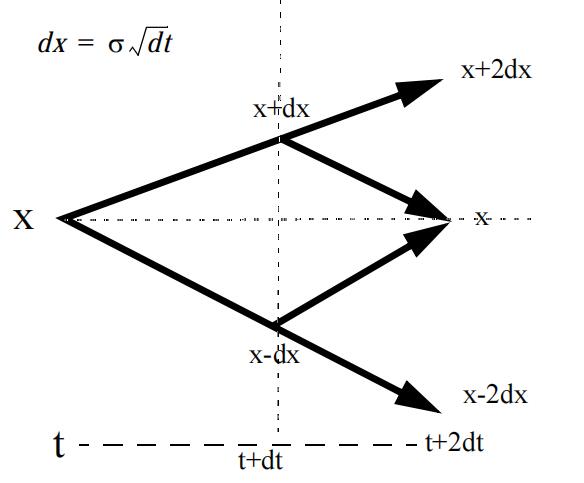

Consider the so-called backward differential equation

¶ s2 ¶ 2

¶tF(x, t) + —–¶x2 F(x, t) = 0

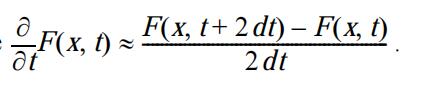

[1.1]for a function F(x, t) . Rewrite this equation as an approximate difference equation on a two-step 微分方程代写

binomial x, t

lattice with all transition probabilities = 1/2, as follows:

Then we can approximate

(i)Assuming dx = sdt , use values of the function on the lattice to show that approximately

(ii)Write down the discrete difference equation that corresponds to Equation [1.1] and explain why it represents abackward [10 points] 微分方程代写

Problem 2. [20 points] 微分方程代写

Suppose that y is the continuously compounded yield to maturity (i.e. discount factor is e–yt ) on a perpetual government bond B that pays $1 per year continuously at constant rate (i.e. cash flow is 1dt during time dt) for every year in the future.

(i)Showthat B(y) 1

(ii)Suppose that the yield y follows the mean-reverting process dy=

a(m – y)dt + bydZ ; where 微分方程代写

a, m and b are all positive constants and Z is a Wiener process. Use Ito’s Lemma to find an expression (in terms of y, m, a, and b) for the expected total return per unit time (the increase in value dB of bond plus value of the interest earned dt, divided by the value of the bond itself) to the owner of the bond? [15]

Problem 3. [15 points] 微分方程代写

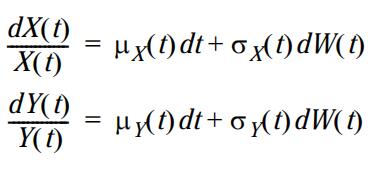

Consider two Ito processes X and Y that take the form

where W(t) is a Brownian processes.

For a twice continuously differentiable functions f(t, x, y) Ito’s Lemma for a function of two pro- cesses takes the form

Show that the process G(t) = X(t)Y(t) is a geometric Brownian motion.微分方程代写

Problem 4. [10 points]

Stock A and stock B both follow independent geometric Brownian motions. Changes in any short interval of time are uncorrelated with each other. Does the value of a portfolio consisting of one of stock A and one of stock B follow geometric Brownian motion? Explain your answer.微分方程代写

Problem 5. [20 points] 微分方程代写

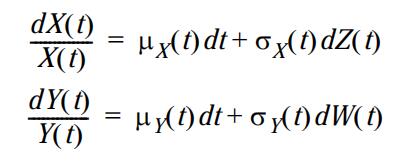

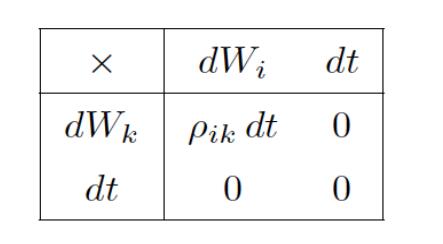

Consider two correlated Ito processes X and Y that take the form

where Z and W are two standard Brownian processes with correlation r so that, in addition to the usual Ito expressions for (dX)2 and (dY)2 , we also have

dZdW =rdt微分方程代写

For a twice continuously differentiable functions f(t, x, y) Ito’s Lemma for a function of two Brownian processes takes the form

Show that the process G(t) = X(t)Y(t) is a geometric Brownian motion, and find the drift m and

the volatility s

of the motion. .You can use the box rule微分方程代写

to compute the drift and variance of a combination of two standard Wiener processes in a sum, and take for granted that the sum of 2 Wiener processes is also a Wiener process.

Problem 6. [15 points]

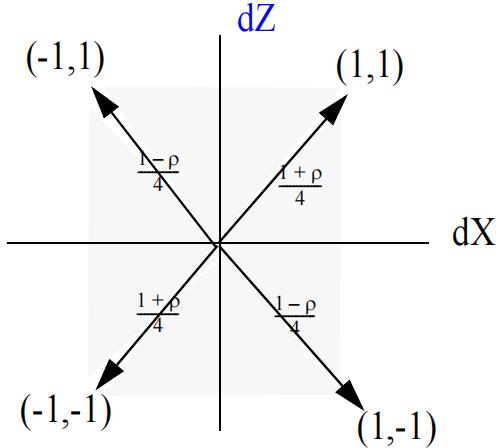

Consider this method discussed in class for generating a double Bernoulli set of increments dX

and dZ such that dX and dZ each take only the values ±1 and have correlation r :

Choose r= –0.5and generate 10,000 successive random steps for dX and dZ.

(i)Plotone path for the cumulative value of X as the number of steps n increases, and one path for the cumulative value of [10]

(ii)Calculate the correlation between the 10,000 dX’s and the 10,000 dZ’s that you[5]

其他代写:web代写 program代写 cs作业代写 analysis代写 app代写 essay代写 assembly代写 Haskell代写 homework代写 java代写 数学代写 考试助攻 web代写 source code代写 finance代写 Exercise代写